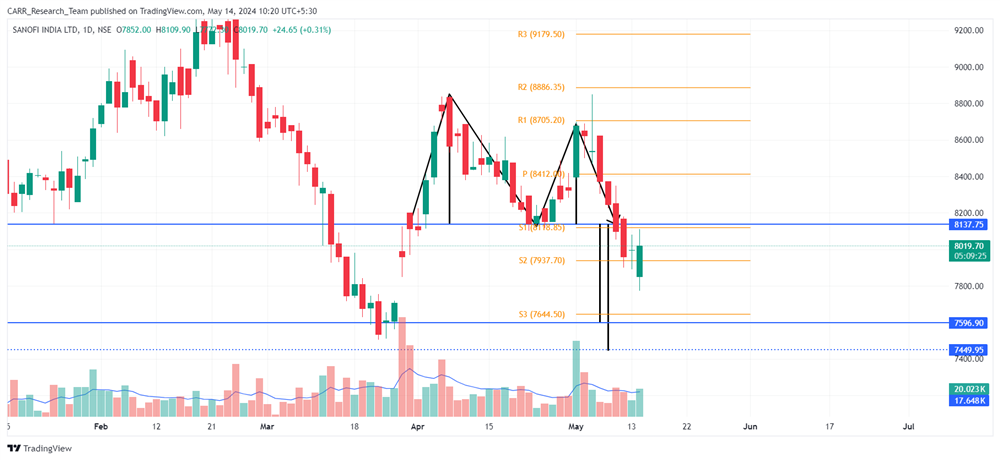

Stock name: Tata Motors Ltd.

Pattern: Double top pattern and retest

Time frame: Daily

Observation:

Post-COVID, the stock experienced a significant upward rally which has recently stabilized. From February to May 2024, it formed a double top pattern on its daily chart and broke out of this pattern on May 16, 2024, with above-average trading volume. After the breakout, the stock retested and moved above the breakout level. Currently, the RSI of the stock is low. According to technical analysis, if the stock loses momentum and falls below the breakout line, it may continue to decline further.

You may add this to your watch list to understand further price action.

Disclaimer: This analysis is purely for educational purpose and does not contain any recommendation. Please consult your financial advisor before taking any financial decision.

Stock name: Hero MotoCorp Ltd.

Pattern: Rounding bottom pattern

Time frame: Monthly

Observation:

From September 2017 to December 2023, the stock formed a rounding bottom pattern on its monthly chart. It broke out of this pattern in December 2023 along with the support of above-average trading volume. Following the breakout, the stock has been rising and maintaining a high RSI level. Technical analysis suggests that if the stock sustains its current momentum, it may continue its upward trend.

You may add this to your watch list to understand further price action.

Disclaimer: This analysis is purely for educational purpose and does not contain any recommendation. Please consult your financial advisor before taking any financial decision.

News for the day:

- Ericsson, the Swedish telecommunications equipment manufacturer, is optimistic about securing 4G and 5G contracts from Vodafone Idea (Vi) following the telecom company's recent equity raise of over Rs 20,000 crore. Nitin Bansal, Managing Director of Ericsson India, shared this optimism in an interview with ET. He also mentioned that Ericsson is considering exporting its 5G equipment from India.

- Karur Vysya Bank plans to open 100 new branches nationwide this financial year, as announced by MD and CEO B Ramesh Babu. The bank's 840th branch was inaugurated in Ayodhya by Chairperson Meena Hemchandra. With a record net profit of Rs 1,605 crore and a net NPA of 0.40% as of March 31, 2024, the bank continues to demonstrate strong growth and asset quality. So far, 39 branches have been opened this year, with the new branch in Ayodhya marking the 35th in the Delhi division.

- Godrej Properties Ltd has sold around 650 flats in Noida, generating over Rs 2,000 crore in revenue, highlighting strong consumer demand for residential properties. The sales came from their newly launched project, Godrej Jardinia, in Sector 146, which debuted in May 2024. This marks Godrej Properties' most successful launch in Noida to date. MD & CEO Gaurav Pandey emphasized the company's plans to expand its presence in Noida, recognizing it as a key market. Godrej Properties is a leading real estate developer with significant operations in the Mumbai Metropolitan Region, Delhi-NCR, Pune, and Bengaluru.

-01_400.png "What is Annual Information statement (AIS)?")