Stock name: ACC Ltd.

Pattern: Triple top pattern

Time frame: Daily

Observation:

Since March 2023, the stock has been on an upward trajectory but has recently stabilized, forming a triple top pattern on its daily chart. On May 10, 2024, it broke out from this pattern, accompanied by average trading volume and a bearish MACD indicator. Additionally, the RSI level of the stock is currently in the lower zone. Based on technical analysis, if the current momentum persists, the stock might experience further downward movement.

You may add this to your watch list to understand further price action.

Disclaimer: This analysis is purely for educational purpose and does not contain any recommendation. Please consult your financial advisor before taking any financial decision.

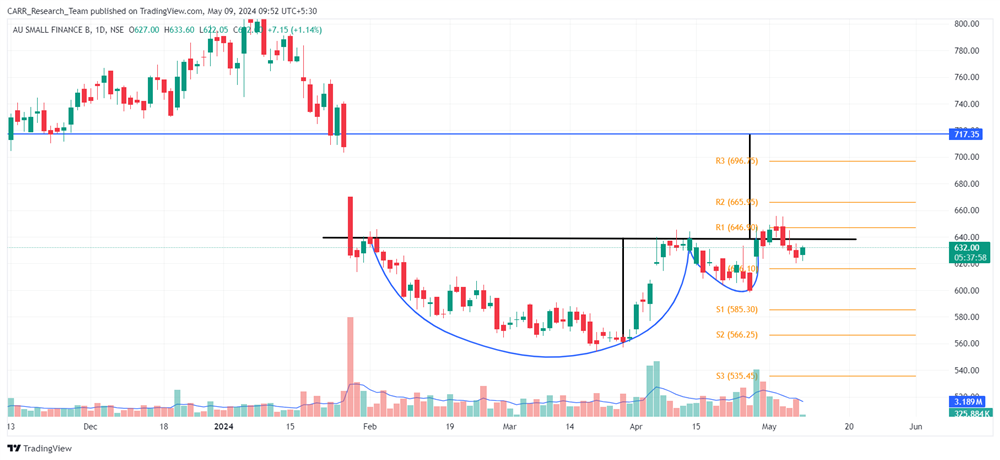

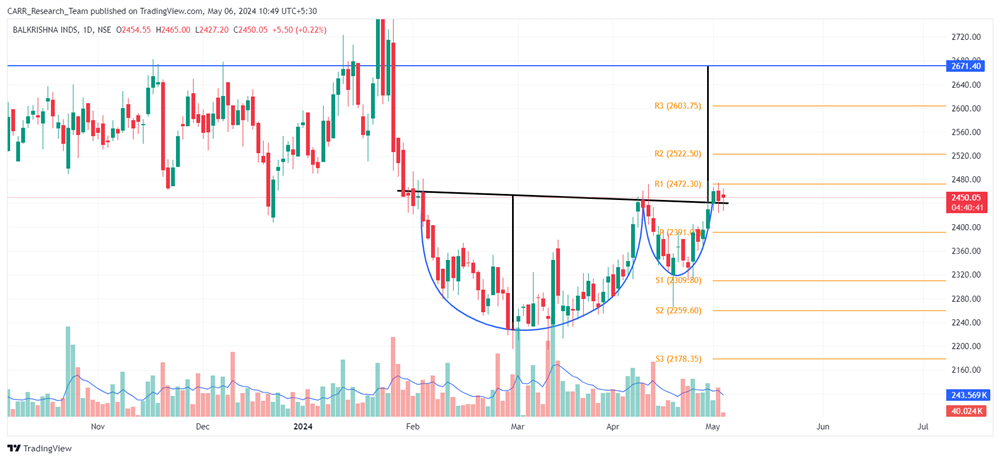

Stock name: Hindalco Industries Ltd.

Pattern: Cup and handle pattern and retest

Time frame: Weekly

Observation:

Between March 2022 and April 2024, the stock underwent a cup and handle formation on its weekly chart, culminating in a breakout in April 2024, accompanied by robust trading volume and a bullish MACD indicator. Presently, the stock is undergoing a retest of this breakout. This has led to cooling of RSI level from the overbought territory. Technical analysis suggests that a successful rebound from this retest may propel the stock in an upward trajectory.

You may add this to your watch list to understand further price action.

Disclaimer: This analysis is purely for educational purpose and does not contain any recommendation. Please consult your financial advisor before taking any financial decision.

News for the day:

- Escorts Kubota Ltd plans to invest Rs 4,500 crore over 3-4 years in a new plant in Ghiloth, Rajasthan, aiming to double tractor production capacity to 3.4 lakh units annually and introduce new engine and construction equipment lines. Land procurement begins this fiscal year, with construction to start by year-end.

- The Hinduja Group has received IRDAI approval to acquire Reliance Capital's insurance businesses, with a condition against pledging shares. However, approvals from RBI and CCI are pending. The NCLT has approved a resolution plan by Hinduja's IIHL, directing payment by May 27, subject to further clearances. IIHL aims to close the transaction soon, awaiting additional regulatory approvals.

- The auditor of Zomato's subsidiaries, Batliboi & Associates, has resigned, prompting the appointment of Deloitte Haskins & Sells LLP for a more streamlined audit process. Zomato aims to align the statutory auditor of its subsidiaries with that of the holding company, enhancing efficiency. The resignation comes ahead of Zomato's board meeting to approve results for the fourth quarter and fiscal year ending March 2024, scheduled for Monday.